You’ve never heard of the name J. Howard Pew before.

Don’t worry, you’re not alone. Truth is, most people haven’t.

Back in 1967, he ran a little company named Sun oil, but you may recognize that company by another name — Sunoco.

One morning that year, this 85-year-old man found himself standing in front of a crowd at a brand-new industrial plant in the middle of the northern Alberta forest, six hours by car from the nearest real city.

You see, Pew had just spent the better part of a decade betting his company’s future on a project that almost every other major oil executive in North America thought was insane — a plant that would dig sandy black tar out of the ground, cook the bitumen out of it, and turn it into synthetic crude.

The plant was called Great Canadian Oil Sands, and it was the first commercial oil sands operation in the world.

And for years, this operation lost money.

But that afternoon Pew told the crowd, “No nation can long be secure in this atomic age unless it be amply supplied with petroleum.”

Unfortunately, Pew died just four years later.

However, Sun Oil invested nearly $250 billion in the Great Canadian Oil Sands project in Fort McMurray, which eventually merged to form Suncor in 1979.

Today, his legacy is one of the largest producers today that has helped Canadian output climb over 5 million barrels per day.

And the world is finally paying him back.

Two Coasts, Two Buyers

The barrels being tapped in the Canadian oil sands is the most important global supply story you’ll never hear about.

But in today’s clickbait environment, the headlines are focused elsewhere.

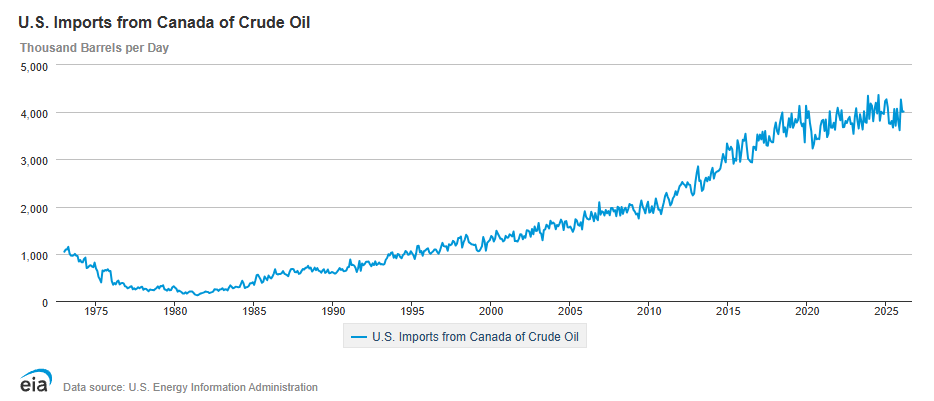

The problem for decades has always been that Canadian producers really only had one customer — the United States.

And believe me, we took full advantage of that fact.

Here’s a quick look at our never-ending thirst for more Canadian barrels:

Today, we’re buying more than four million barrels per day from Canada.

That makes sense, right? You see, up until recently, the only way to get that Canadian crude out of northern Alberta was through pipelines to the U.S. We were essentially locked in as Canada’s best customer for decades.

It was a win-win situation for U.S. refiners, because the lack of competition for heavy Canadian crude meant they could buy it at a reasonable discount to WTI. Of course, that’s not to mention the fact that those refineries along the Gulf Coast were specifically tailored to process heavy crude.

However, those barrels of heavy Canadian crude finally have somewhere else to go.

Two years ago, the Trans Mountain Expansion came online, and effectively tripled Canada’s West Coast export capacity to 890,000 bpd.

Tanker loadings at Westridge Marine Terminal in Burnaby went from one a month before TMX to roughly one a day by late 2025 — with about 80% of those barrels bound for Asia.

Rongsheng Petrochemical’s 800,000-bpd Zhejiang refinery in China now treats Canadian heavy as its preferred non-sanctioned alternative to Russian crude.

Meanwhile on the U.S. Gulf Coast, the price action has completely flipped.

In April 2026, Canadian heavy traded at a $13.55 premium on the Gulf Coast — the widest in over two years — as the contested Strait of Hormuz and the collapse of Venezuelan exports forced refiners to bid up secure supply.

Canada is now the single biggest source of heavy crude into the Gulf Coast at 13.6 million barrels per month.

Now look at the alternative…

Venezuelan output peaked at 3.4 million bpd in the early 2000s.

Today it produces about 800,000 bpd.

And no matter what delusional rhetoric we see in today’s headlines, the cold, bitter truth here is that PDVSA is in both financial AND operational ruin — that’s S&P’s language, not mine — with capital flight, lost technical expertise, and decayed infrastructure that has not been seriously maintained in twenty years.

Rebuilding to a competitive 4 million bpd would take an estimated $100 billion in capex and at least a decade.

Folks, that’s simply not going to happen — at least, not in today’s environment.

Remember, ExxonMobil and ConocoPhillips were both expropriated from the Orinoco Belt in February 2007, and spent the next seven years winning ICSID arbitration awards — $1.6 billion and $8.7 billion respectively.

Neither is going back.

Meanwhile, Chevron remains the only U.S. major that stayed.

Yet, even with the post-Maduro political shift and Washington’s political backing, no Big Oil board on Earth is signing off on $20 billion of Venezuelan capex right now — the capital is not coming!

Pew Was Right

When J. Howard Pew opened that first commercial oil sands plant back in 1967, he was 85 years old.

Although he only had three more years to live, he had just bet Sun Oil Company’s future on a project that nobody in the industry believed could ever be commercialized.

Again, he was right.

As I mentioned before, Pew’s project turned into one of the largest oil sands companies today.

Now that the world’s two biggest refining markets — the U.S. Gulf Coast and coastal China — are now paying premium prices to lock up that supply, the only credible alternative source of large-scale heavy crude is functionally non-existent.

This isn’t a tactical trade, dear reader.

The Venezuelan industry isn’t coming back without $100 billion in capex that nobody in the C-suite at Exxon or Conoco or Chevron has any appetite to spend.

Russian oil remains sanctioned, and Mexican heavy crude is shrinking as Pemex pulls barrels for domestic refining.

The only real barrels left standing are Canadian.

And the market is just starting to price it that way.

Right now, my readers and I have found three more Canadian producers that are slated to outperform Big Oil over the next 18 months — including one small-cap tied directly into TMX volumes.

You can see the full list right here.

Until next time,

Keith Kohl

A true insider in the technology and energy markets, Keith’s research has helped everyday investors capitalize from the rapid adoption of new technology trends and energy transitions. Keith connects with hundreds of thousands of readers as the Managing Editor of Energy & Capital, as well as the investment director of Angel Publishing’s Energy Investor and Technology and Opportunity.

For nearly two decades, Keith has been providing in-depth coverage of the hottest investment trends before they go mainstream — from the shale oil and gas boom in the United States to the red-hot EV revolution currently underway. Keith and his readers have banked hundreds of winning trades on the 5G rollout and on key advancements in robotics and AI technology.

Keith’s keen trading acumen and investment research also extend all the way into the complex biotech sector, where he and his readers take advantage of the newest and most groundbreaking medical therapies being developed by nearly 1,000 biotech companies. His network includes hundreds of experts, from M.D.s and Ph.D.s to lab scientists grinding out the latest medical technology and treatments. You can join his vast investment community and target the most profitable biotech stocks in Keith’s Topline Trader advisory newsletter.